Latest News:

Protecting Your Business. Insuring Your Future.

Your Farm

We are proud to protect farms of every size. Because our founders were farmers, and our roots are in the land.

Your Business

If your business is one-of-a-kind, you need an insurance company that offers unique commercial products.

Your Home

Your peace-of-mind is our top priority. Let us help you protect your most-prized possession.

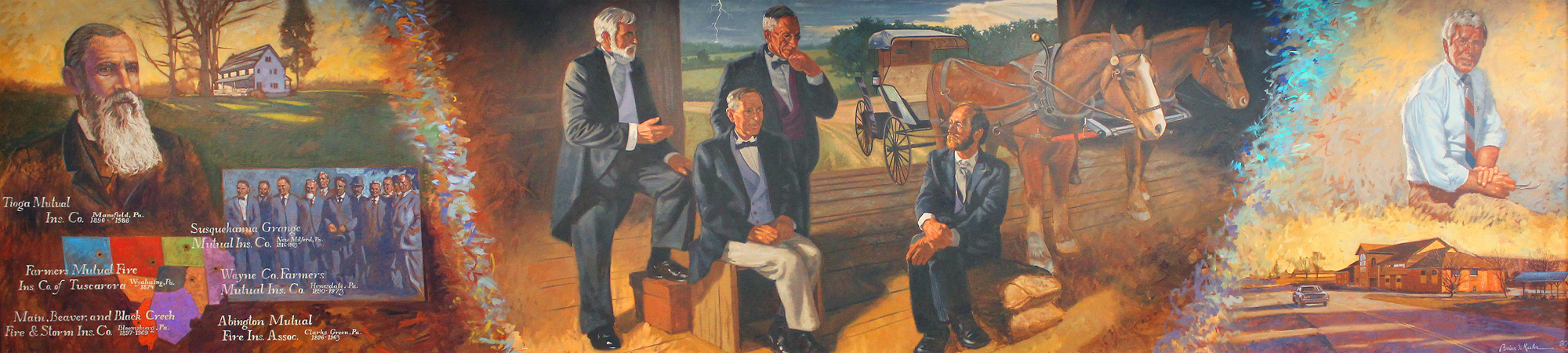

Serving The Underserved Since 1874.